Strategy’s new $1.25B Bitcoin sale plan continues to elicit mixed reactions. Galaxy Research is the latest to weigh in on the monetization framework that the world’s largest Bitcoin treasury firm released earlier this week.

According to Alex Thorn, Galaxy’s Head of Research, the markets “like” the new plan, but cautioned that it does not eliminate the underlying “structural risks.”

This was a smart move by Strategy, but it may not resolve structural issues forever. Strategy still has a large preferred stack, and it still has large recurring obligations.

As part of the plan, Strategy raised $1 billion in cash and formalized a 12-month cash reserve buffer. That effectively provided about 17 months of coverage for its obligations.

Additionally, it approved selling up to $1.25B in BTC to fund the interest obligations.

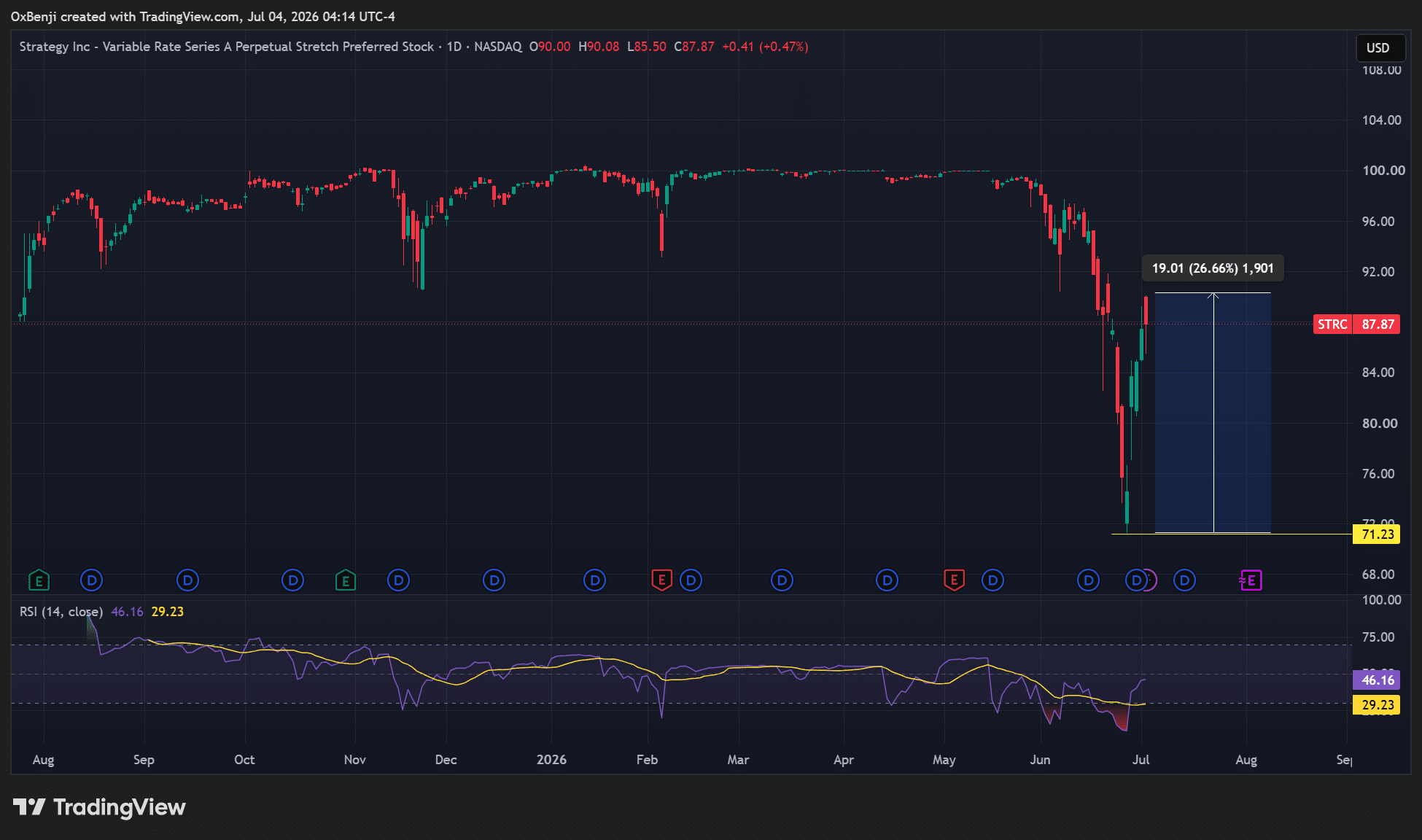

MSTR rallied from $82.5 to $100, while preferred stock STRC jumped 26% from a record low of $71 to $90. Although STRC remained below its $100 peg, Galaxy said the rebound reflected positive market sentiment toward Strategy’s plan.

But Galaxy’s Thorn added that Strategy’s obligations will increase in the next two years as $6.7B in convertibles will be due. He warned that Strategy’s BTC sales would effectively exacerbate MSTR and STRC weakness.

Galaxy’s ‘middle ground’ proposal to Strategy

For Thorn, apart from cash reserves, MSTR and BTC sales, there is a fourth option that can address Strategy’s cash-flow concern.

A company with 847,363 BTC should not let a temporary cash-flow concern become an existential narrative crisis. Strategy should explore generating income from the BTC stack without necessarily selling spot BTC.

Thorn said this could be in the form of BTC lending or options strategies on a limited amount of BTC. This would reduce other issues like counterparty risk. In fact, Metapanet has leveraged options strategies for cash flow and BTC accumulation.

The analyst concluded that this was a ‘middle ground’ that does not dilute MSTR holders and sell BTC, which should also be considered.

This was different from JPMorgan analysts, who recommended increasing the cash reserve buffer from 17 months to 2 or 3 years by selling more MSTR, not its BTC holdings.

Galaxy’s proposal seemed apt because it’s been tested by Metaplanet. And it would not affect MSTR and BTC holders. It would also raise more cash flow to cover Strategy’s obligations if the risks are well managed.

Final Summary

- Galaxy urged Strategy to consider using a limited amount of its BTC for cash income generation instead of selling BTC or MSTR dilution.

- However, JPMorgan proposed increasing the cash buffer up to 2-3 years by selling more MSTR, but not its BTC stash

{kind=link}